Keywords: M&A, takeover, PAC, Creeping acquisition, open offer,

public announcement

[Anjana Ravikumar is a III Year B.B.A.LL.B student at Gujarat National

Law University (GNLU)]

INTRODUCTION

Since the advent of globalization, the

doors of the Indian economy have been open for overseas investors. To

compete on a global platform, companies have to continuously amplify the

scale of their business. Mergers and Acquisitions (“M&A”) pave the way

for a suitable option to capture the opportunities created by such

policies.

BACKGROUND

One of the earliest takeovers in India can be traced back to the

acquisition of Pukhuri Tea Co. Ltd. by Bishnauth Tea in 1965. However, the

waves of corporate deal-making swept the Indian landscape during the

1980s, which witnessed tentative reforms under the Rajiv Gandhi

administration. The first hostile takeover attempt was made out by the

London based industrialist,

Swaraj Paul in 1983.

A

takeover is an acquisition of control of a registered company through the

purchase or exchange of shares. A

Merger on the other hand involves

the amalgamation of two or more companies either through the exchange of

shares or the formation of a new company. Thus, while mergers involve an

amalgamation through mutual consent of the companies, acquisitions or

takeovers may either be friendly or hostile. Further, in an acquisition,

the target company is engulfed by the acquirer and hence ceases to exist,

while in a merger it is the fusion of two or more companies into one new

entity.

Takeovers have been associated with

propelling economic efficiency.

However, it has a tendency for being exploited as a weapon, at the

disposal of corporate raiders with massive capital resources, often

prejudicial to the interests of retail investors. To prevent such

exploitation and encourage the growth of the securities market, SEBI was

established in 1992 as a regulatory body.

Subsequently, the

SEBI (Substantial Acquisition of Shares and Takeover [SAST]) Regulations,

1997 were formulated; incorporating the suggestions of the PN Bhagwati

Committee. These were substituted by the SEBI (Substantial Acquisition of

Shares and Takeover) Regulations in 2011 (hereinafter “Takeover Code”).

based on the recommendations of the Takeover Regulations Advisory

Committee (“TRAC”) headed by Mr. C. Achuthan.

IMPORTANT TERMINOLOGIES:

Persons acting in concert (“PACs”):

According to Regulation 2(1)(q) of the Takeover Code,

PACs are persons who, in

furtherance of a common objective or purpose of substantial acquisition of

shares, voting rights, or gaining control over the target company. The

same is done pursuant to a formal or informal agreement or an

understanding which is pertaining to either directly or indirectly

co-operating in acquiring, agreeing to acquire shares, voting rights or

control of the target company. The question regarding whether two persons

constitute PACs is to be answered based on an analysis of the

facts and circumstances of the

case.

The

scope of PAC has been broadened to

include a new class known as deemed PACs under regulation 2(1)(q)(2) of

the latest Takeover Code. Deemed PACs include promoters, immediate

relatives, trustees, a collective investment scheme and its company,

venture capital fund, and its sponsor and asset management company.

However, deemed PACs will be considered after the abovementioned PACs as

acting in concert.

Acquirer

An

acquirer is defined under

regulation 2(1)(a) of the Takeover

Code. Any person who by himself or through or with PACs, directly or

indirectly acquires or agrees to acquire, shares, voting rights or control

of the target company is called an acquirer. An acquirer may be a natural

person, a corporate entity, or any other legal entity.

DISCLOSURE REQUIREMENTS:

To ensure that the price discovery of shares of the target company takes

place in an informed manner, several disclosures have been made mandatory

under Chapter V of the Takeover

Code. The disclosures required are:

- Disclosure of acquisition and

disposal: It is required for all acquirers to disclose acquisitions of 5%

or more voting rights of the target company within two working days after

such acquisition. The disclosure must be made to every stock exchange

where the shares of the company are listed and to the registered office of

the target company. The same does not apply to a scheduled commercial bank

or a public financial institution.

- Continual disclosures: If any

acquirer along with his PACs holds shares or voting rights entitling him

to exercise 25% or more of voting rights in the target company, he is

required to disclose the same. Further, every promoter along with his PACs

is required to disclose their aggregate shareholding and voting rights in

the form as specified in the Regulations.

- Disclosure of encumbered

shares: The promoter along with his PACs shall disclose details regarding

any shares encumbered by them or any release or invocation of such

encumbered shares to the stock exchange and the target company’s

registered office within seven working days.Disclosure requirements thus,

seek to protect the interest of the public stakeholders by ensuring

transparency.

OPEN OFFER:

An open offer under the

Takeover Code is an offer made by an acquirer to the shareholders of the

target company inviting them to tender their shares at a particular price.

It provides an exit option to the shareholders of the target company

during a change in control or substantial acquisition of shares in the

target company. Thus, open offer provides the public shareholders an

opportunity to withdraw their investment when there is a change in the

management or promoter shareholding.

The Takeover code

stipulates clearly that not just direct but even indirect acquisitions of

shares, voting rights or control will trigger an open offer. Indirect

acquisition is defined under

regulation 5(1) of the Takeover

Code. It includes any acquisition of shares, voting rights in or control

over any company which enables the acquirer and PACs, to exercise or

direct the exercise of control over or voting rights in the target

company. Such acquisition is made without attracting the obligation to

make an announcement of public offer.

To protect the economic

interests of the exiting shareholders of the target company, it has been

made mandatory for the offer to be at the best possible terms for the

shareholders. To ensure the same, the Takeover Code prescribes the timing,

minimum offer size, price discovery mechanisms, etc. An open offer may be:

Mandatory Open Offers: The Takeover Code prescribes

certain circumstances under which an acquirer is obliged to issue a

mandatory tender offer to the existing shareholders of the target company

to acquire at least a minimum of 26% of its shares. The triggers/

circumstances include:

-

Initial Trigger – When the acquirer along with his PACs plans

to acquire shares which allows them to exercise 25% or more of the

voting rights in the company.

-

Consolidation Trigger – When acquirer and PACs together hold

25% or more of shares or voting rights but it is less than the maximum

permissible limit of non-public shareholding in a target company.

-

Control Trigger – When an acquirer gains control over the

target company, irrespective of shares owned.

-

Trigger on Indirect Acquisition – When an acquirer indirectly

acquires the ability to exercise voting rights or control over target

company as specified in initial, consolidation, or control triggers.

Voluntary Open Offer: A voluntary offer is made by an existing

shareholder or an acquirer who holds no shares. Under

Regulation 6 of the Takeover Code,

a voluntary offer is to be made when the acquirer and PACs exercise a

minimum of 25% or more of voting rights but less than the maximum limit of

non-public shareholding in the target company. Voluntary offers have to be

made for a minimum of 10% of the total shareholding of the target company.

Competing Offer: The Takeover Code under

Regulation 20 permits third

parties to make offers to the shareholders providing exit opportunities

while the acquirer’s open offer subsists. This creates orderly competition

among acquirers.

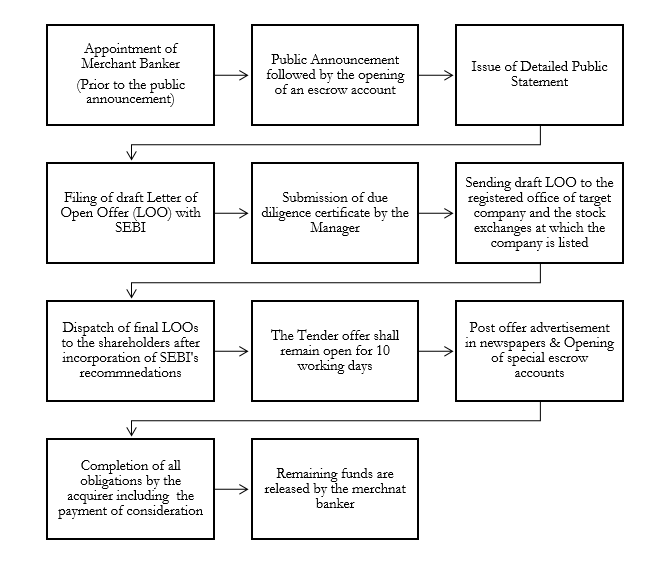

PROCEDURE OF AN OPEN OFFER:

The major steps involved in the

open offer process are as follows:

CREEPING ACQUISITION:

· Covered under Regulation 3(2)

of the Takeover Code,

Creeping Acquisition is a means to

facilitate the consolidation of shares, voting rights, or control in the

company by persons already holding or controlling a substantial number of

shares.

· Under this provision, acquisition of voting shares

in a listed company; without public announcement; in excess of 25%, is

permissible provided that the acquisition is limited to 5% in one

financial year.

· Every financial year, an additional 5%

voting rights can be acquired by an acquirer with PACs. However, this

additional acquisition via creeping acquisition can only extend up to a

total shareholding of 75% of the share capital.

· Beyond this

75% limit, a public announcement is mandatory. The

5% limit is to be calculated by

aggregating all purchases, without including the aggregate sales.

EXEMPTIONS FROM OPEN OFFERS:

The exemptions

applicable to open offers are dealt with under

Regulation 10 and 11 of the

Takeover Code. Circumstances under which a company is exempt from the

issue of open offer include:

1. Inter se Transfers: Inter se transfers occur between immediate

relatives, between a company and its subsidiaries, holding company and

other subsidiaries of such holding company are exempt from the obligation

of issuing open offer. Transfer to PAC for three years or more, prior to

the proposed acquisition is also exempted.

Regulation 10(1)(a)(ii)

of the Takeover Code provides for inter se transfer amongst promoters

which can be exempted only if the said promoter holds shares for at least

three years, prior to such acquisition. Inter se transfers are exempt from

the obligation of open offer since there is no change in ownership per se.

2. Trusts: The transfer of shares to trusts are exempt

from the obligation of open offer under the following conditions:

-

Such transfer shall not affect the ownership or control of shares or

voting rights in the target company.

-

The trust is a mirror image of the promoter holding such shares.

-

Only individual promoters, immediate relatives, or lineal descendants

can be the beneficiaries of the trust.

-

The beneficial interest shall not be transferred, assigned, or

encumbered.

-

After dissolution, the assets can be transferred only to beneficiaries

or their legal heirs.

-

The trustees cannot transfer or delegate their powers.

3. Intermediaries: The transfer of shares in return for services

rendered are exempt from the obligation of open offer. Intermediaries

include underwriters, stockbrokers, merchant bankers, registered stock

marker, and scheduled commercial banks acting as an escrow agent.

4. Insolvency and Bankruptcy: The acquirers of

distressed companies are not obliged to make an open offer. The

acquisitions of

Bhushan Steel by Tata Steel is one

such acquisition under IBC which was exempted from open offer

obligation.

5. Disinvestment: Defined under

Regulation 2(g) of the Takeover

Code, disinvestment is the direct or indirect sale by the Central/State

Government or by a government company of shares, voting rights or control

over a target company, which is a public sector undertaking. Acquisition

of shares during disinvestment is exempt from the obligation of open

offer.

6. Investment Funds: Alternate Investment Funds

and Venture Capital Funds are exempted from making an open offer, when

their investments cross the threshold which triggers an open offer.

7. Buyback of shares: If the

buyback of shares results in an

increased shareholding of the promoter, it will not trigger an open offer.

8. Forfeiture of shares: Increase in voting rights of

existing shareholders due to forfeiture of partly paid shares and

non-payment by defaulting shareholders does not necessitate the issue of

an open offer.

9.

Acquisition under the SARFAESI Act, 2002: The Securitisation and

Reconstruction of Financial Assets and Enforcement of Security Interest

Act, 2002 (SARFAESI) vests in banks the power to auction properties of

borrowers who default the loan payment.

Asset Reconstruction

Companies acquiring financial assets from banks and other financial

institutions are duty-bound to return them upon recovery of the amount.

Such acquisitions under SARFAESI Act, therefore, fall within the ambit of

exemption from open offers.

Acquisitions by way of

transmissions, inheritance, succession, rights issue, and exchange of

shares also fall within this exemption. When the company is unsure about

the exemption of a proposed transaction, it may seek informal guidance

from SEBI through an application. Further, SEBI also has the discretionary

power to grant exemptions for specific transactions, in the interest of

the stakeholders of the company though not provided for in the code.

PUBLIC ANNOUNCEMENT:

When the acquirer

acquires voting rights of the target company, in excess of limits

prescribed under

Regulation 3 and 4 of the Takeover

Code, the acquirer is required to give a Public Announcement of Open offer

to the shareholders of the target company.

It contains details

about the offer, the acquirer(s)/PAC, the transaction which triggered the

open offer or the underlying transaction details of selling shareholders

(if any), the target company, and the price and mode of payment. It is the

first announcement made by the acquirer disclosing details of the

intention to acquire the shares of the target company from existing

shareholders through an open offer.

Public Announcement is

issued on behalf of the acquirer, by the Manager to the offer, in the

format as provided under

Regulation 15(1)

of the Takeover Code. The Takeover Code also prescribes a specific

timeline for Public Announcement. Public announcements are essential to

safeguard the interests of the shareholders.

DETAILED PUBLIC STATEMENT (DPS):

The DPS is the second announcement made by the acquirer and

the PACs disclosing all relevant information regarding the open offer. It

enables the shareholders to make an informed decision regarding the open

offer. Under Regulation 13(4) of

the Takeover Code, a DPS shall be published by the acquirer through the

manager to the offer within a maximum of five working days from the date

of Public Announcement.

Regulation 15(2) of the Takeover

Code provides the format for the Detailed Public Statement.

LETTER OF OPEN OFFER (LO):

After the publication of Detailed Public Statement (DPS), within 5 days,

the acquirer through the manager of the offer is required to file a draft

letter of offer with SEBI. SEBI is required to revert with its comments on

the LO within 15 working days. SEBI oversees that the disclosures

contained in the LO are adequate and in conformity with the Regulations.

Once approved by SEBI, it is dispatched to the shareholders of the target

company as on an identified date.

While the PA and the DPS are

made by the acquirer to inform the public of an exit opportunity available

to them, the LOO is an offer made by the acquirer to the identified

shareholder of the target company to purchase their shares.

CONCLUSION:

Although not all corporate takeovers may be deemed beneficial to the

economy, an overwhelming majority of them are economically justifiable and

are not mere opportunistic managerial power-grabs. SEBI has constantly

strived to curb undesirable practices and protect the interests of

investors to encourage mergers and takeovers.

The new Code

based on the suggestions of the TRAC has relied on court rulings,

International Takeover Codes, and sound statistical analysis to plug all

loopholes. It aims to provide clarity by simplifying and aligning with

internationally accepted practices.

The ever-evolving public

M&A landscape continues to throw new challenges for SEBI to address.

However, the new Takeover Code presently is at par with any foreign code

on mergers and acquisitions and continues to ensure a systematic and

transparent mechanism for takeovers in India.

-By Anjana Ravikumar